401k: A Smart Path to Retirement Wealth

💡Introduction: What Is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that helps you invest a portion of your paycheck for the future—with major tax benefits. Whether you're planning early or catching up on savings, a 401(k) offers one of the best paths to financial freedom in retirement.

🔍 How a 401(k) Works

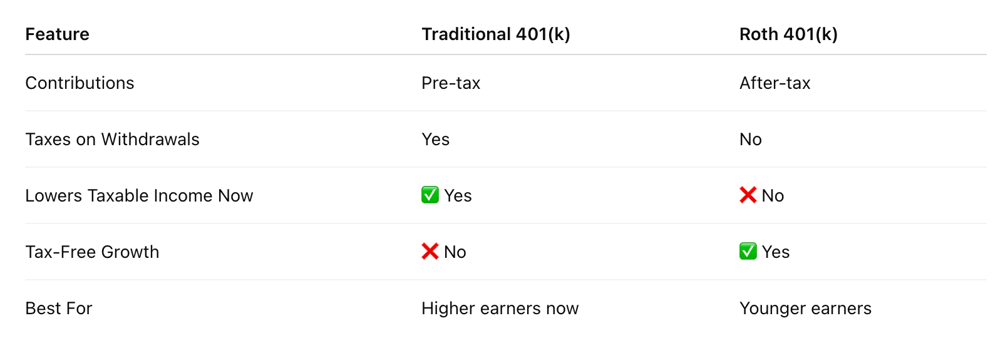

Pre-tax contributions (Traditional 401(k)) lower your taxable income today.

After-tax contributions (Roth 401(k)) allow for tax-free withdrawals in retirement.

Your contributions grow tax-deferred over time.

Many employers offer matching contributions, adding free money to your retirement pot.

🎯 Key Benefits

✅ Tax Efficiency – Reduce taxes now (Traditional) or later (Roth)

✅ Employer Match – Get up to 100% match on part of your contributions

✅ Higher Contribution Limits – Save more than with IRAs

✅ Automatic Saving – Contributions deducted straight from your paycheck

📌 2025 Contribution Limits

Under age 50: $23,000

Age 50 or older: $30,500

👉 Check the IRS site for updated limits

📈 Growth Potential Example

Contribute $500/month for 30 years at a 7% return = $600,000+

Add a 50% employer match? You may reach $900,000+

⚖️ Traditional vs Roth 401(k) (Comparison)

🧮 401k Calculator

Use 401k Calculator to calculator to determines the value of your 401(k) account over time.

🔁 Rules, Withdrawals, and Penalties

Early Withdrawal Penalty: 10% + income tax if withdrawn before age 59½

RMDs: Required from age 73 (Traditional 401(k) only)

Loans: Some plans allow borrowing, but with trade-offs

🛠️ Best Practices to Maximize Your 401(k)

💰 Get the Full Employer Match – Don’t leave free money on the table

📈 Increase Contributions Over Time – Aim for 10–15% of your salary

🧾 Choose Low-Fee, Diversified Funds – Index and target-date funds are solid options

⏳ Avoid Early Withdrawals – Let compounding work its magic

🚪 No 401(k)? Explore Alternatives

If your employer doesn’t offer a 401(k), you can still save with:

Traditional or Roth IRA

SEP IRA for self-employed

Solo 401(k) for freelancers/business owners

❓ Frequently Asked Questions (FAQs)

Q: Can I contribute to both a 401(k) and an IRA?

Yes, you can contribute to both, though income limits may affect IRA deductibility.

Q: What happens to my 401(k) when I switch jobs?

You can leave it, roll it into a new employer’s plan, or move it into an IRA.

Q: Should I choose Roth or Traditional?

It depends on your current tax bracket vs. your expected retirement bracket. Many choose both to diversify.

🧠 Final Thoughts

A 401(k) is more than a savings account—it’s a vehicle for financial independence. With the right approach, you can take full advantage of tax benefits, compounding, and employer contributions to retire on your own terms.

Disclaimer: The information provided on InvestmentIntro.com is for educational and informational purposes only. It should not be considered financial, investment, or tax advice. We are not licensed financial advisors or tax professionals. You should consult with a qualified financial advisor or tax professional before making any financial decisions. All content is provided “as is” without any representations or warranties.

about us | terms of use | privacy policy | contact us

© 2025. All rights reserved.