Overview of Tax-Advantaged Accounts

Saving and investing are key components of long-term financial success, but how you structure those investments can significantly affect your wealth over time. That’s where tax-advantaged accounts come into play. These accounts are designed to encourage saving for retirement, education, and health expenses by offering tax benefits that can improve your overall returns and reduce your tax burden.

In this guide, we’ll cover the major types of tax-advantaged accounts available in the United States, their benefits, and considerations for choosing the right ones based on your financial goals.

What Are Tax-Advantaged Accounts?

Tax-advantaged accounts are investment or savings accounts that receive preferential treatment under the U.S. tax code. These advantages can include:

Tax deductions on contributions

Tax-deferred growth, where earnings aren’t taxed until withdrawn

Tax-free growth, where earnings and withdrawals are entirely tax-free

These benefits allow your money to compound more efficiently over time and are particularly valuable when saving for long-term goals.

Major Types of Tax-Advantaged Accounts

Retirement Accounts

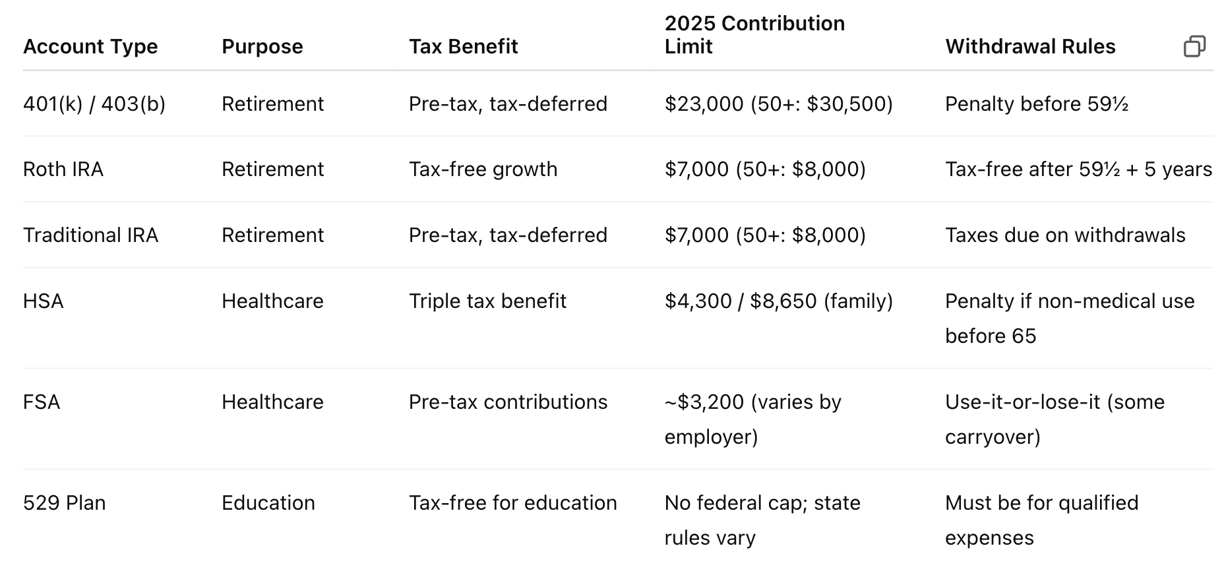

401(k) and 403(b)

Who qualifies: Employees of for-profit (401k) or nonprofit/government (403b) organizationsContribution limit (2025): $23,000 (under 50), $30,500 (50+)

Key benefits:

Pre-tax contributions reduce your taxable income

Employer match is free money

Tax-deferred growth

Taxation: Withdrawals taxed as ordinary income in retirement

Roth 401(k)

Similar structure to a traditional 401(k), but contributions are after-tax

Earnings grow tax-free, and qualified withdrawals are tax-free

Traditional IRA

Contribution limit: $7,000 (under 50), $8,000 (50+)

May be tax-deductible depending on income and workplace retirement plan coverage

Tax-deferred growth

Withdrawals taxed as income in retirement

d. Roth IRA

Funded with after-tax dollars

Tax-free growth and tax-free withdrawals in retirement

Income limits apply for eligibility

Great for young investors who expect to be in a higher tax bracket later

Health Savings Account (HSA)

Key benefits:

An HSA is a triple tax-advantaged account available to individuals with high-deductible health plans (HDHPs).

Contributions are tax-deductible

Growth is tax-deferred

Withdrawals for qualified medical expenses are tax-free

Can be used as a supplemental retirement account if not used for medical expenses

Contribution limit (2025): $4,300 individual / $8,650 family

Education Savings Accounts

529 College Savings Plan

Allows contributions to grow tax-free

Withdrawals for qualified education expenses (tuition, books, etc.) are tax-free

No income limit on contributions

Some states offer state tax deductions or credits

Coverdell ESA (Education Savings Account)

More flexible than a 529 in terms of investment choices

Contribution limit: $2,000 per year per beneficiary

Income limits apply for contributors

Can be used for K–12 and higher education

Flexible Spending Account (FSA)

Offered by employers; use-it-or-lose-it account for health-related expenses

Tax-deductible contributions

Withdrawals for medical expenses are tax-free

Less flexible than an HSA (no rollover, not portable)

Benefits of Using Tax-Advantaged Accounts

Faster Wealth Accumulation

You keep more of your returns by deferring or avoiding taxes entirely.Reduced Taxable Income

Contributions to traditional retirement accounts or HSAs can lower your current tax bill.Goal-Specific Planning

These accounts help earmark money for retirement, healthcare, or education, keeping your finances organized and purpose-driven.

Key Considerations

Withdrawal Rules: Many accounts penalize early withdrawals (typically before age 59½ for retirement accounts).

Contribution Limits: Limits change yearly, so staying updated ensures you maximize benefits.

Eligibility Requirements: Income thresholds and employment status can affect your ability to contribute.

Account Fees and Investment Options: Not all plans are created equal—compare fees, investment options, and flexibility.

Tax-Advantaged vs. Taxable Accounts

Taxable brokerage accounts offer flexibility and no contribution limits, but earnings are subject to capital gains taxes and dividends are taxed annually. While they’re useful for excess savings or short-term goals, tax-advantaged accounts offer clear benefits for long-term wealth building.

Which Should You Prioritize?

Employer 401(k) up to match – Free money; take it!

Roth IRA or Traditional IRA – Tax-free or tax-deferred growth depending on your income and future tax bracket expectations.

HSA – If eligible, this can double as healthcare and retirement savings.

529 Plan – If you have children and want to save for their education.

Taxable account – After maximizing tax-advantaged accounts.

Summary Table

Final Thoughts

Understanding and using tax-advantaged accounts is a cornerstone of effective personal finance. Whether you're planning for retirement, future healthcare needs, or your child’s college education, taking advantage of these accounts can lead to significant tax savings and long-term growth. The earlier you start, the more you benefit from compounding and reduced taxes. Explore your options, and build your financial future with tax efficiency in mind

Disclaimer: The information provided on InvestmentIntro.com is for educational and informational purposes only. It should not be considered financial, investment, or tax advice. We are not licensed financial advisors or tax professionals. You should consult with a qualified financial advisor or tax professional before making any financial decisions. All content is provided “as is” without any representations or warranties.

about us | terms of use | privacy policy | contact us

© 2025. All rights reserved.