Roth IRA: Tax-Free Future for Smart Investor

What Is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a retirement savings account that allows you to contribute after-tax dollars, with the key benefit of tax-free growth and tax-free withdrawals in retirement. Unlike a Traditional IRA, where contributions may be tax-deductible but withdrawals are taxed, the Roth IRA flips the model: you pay taxes now, and enjoy tax-free income later.

Key Features of a Roth IRA

✅ Contribute with after-tax income

📈 Tax-free growth on investments

💰 Tax-free qualified withdrawals after age 59½

🚫 No Required Minimum Distributions (RMDs)

💼 Ideal for those expecting to be in a higher tax bracket in retirement

Contribution Limits

For 2024, the contribution limits are:

Under age 50: $7,000

Age 50 or older: $8,000 (includes $1,000 catch-up contribution)

💡 Check the IRS for the latest contribution limits.

Income Eligibility

Roth IRA contributions are phased out based on income:

Single filers: Income must be below $146,000 (2024 phase-out starts at $138,000)

Married filing jointly: Income must be below $230,000 (2024 phase-out starts at $218,000)

If your income exceeds these limits, you may consider a Backdoor Roth IRA strategy.

Benefits of a Roth IRA

🛡️ Tax-Free Retirement Income: Withdrawals after age 59½ and after holding the account for at least 5 years are 100% tax-free.

🔄 Flexibility: You can withdraw your contributions (not earnings) at any time, tax- and penalty-free.

🧓 No RMDs: Unlike Traditional IRAs and 401(k)s, Roth IRAs do not require withdrawals at any age, giving you more control and estate planning flexibility.

🧠 Great for Younger Investors: The earlier you contribute, the more time your money has to grow tax-free.

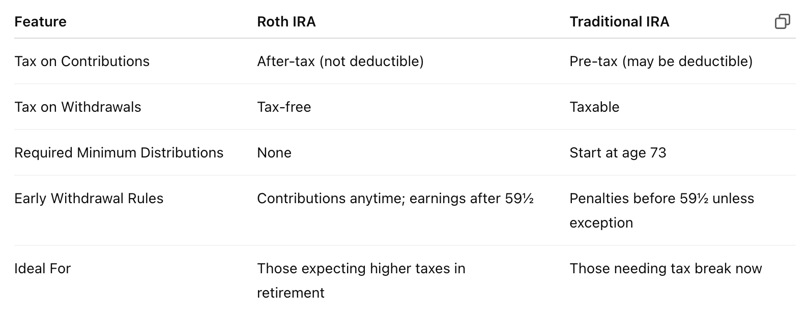

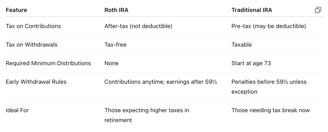

Roth IRA vs. Traditional IRA

Feature Roth IRA Traditional IRA Tax on Contributions After-tax (not deductible) Pre-tax (may be deductible) Tax on Withdrawals Tax-free Taxable Required Minimum Distributions None Start at age 73 Early Withdrawal Rules Contributions anytime; earnings after 59½ Penalties before 59½ unless exception Ideal For Those expecting higher taxes in retirement Those needing tax break now

Who Should Consider a Roth IRA?

Young professionals in a lower tax bracket

People who value tax-free income in retirement

Individuals who want to avoid RMDs

Anyone with access to earned income under income limits

Opening a Roth IRA

You can open a Roth IRA with most financial institutions, including:

Brokerages (Fidelity, Vanguard, Charles Schwab)

Robo-advisors (Betterment, Wealthfront)

Banks and credit unions

Look for low fees, strong investment options, and intuitive platforms.

Use This Calculator to Plan

👉 Roth IRA Calculator – SmartAsset

Final Thoughts

The Roth IRA is a powerful investment tool that rewards patience and long-term planning. It provides a unique opportunity to lock in today’s tax rate and enjoy tax-free income for life. Whether you're just starting your financial journey or looking to diversify your retirement plan, the Roth IRA deserves a place in your portfolio.Roth IRA: Tax-Free Future for Smart Investors

What Is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a retirement savings account that allows you to contribute after-tax dollars, with the key benefit of tax-free growth and tax-free withdrawals in retirement. Unlike a Traditional IRA, where contributions may be tax-deductible but withdrawals are taxed, the Roth IRA flips the model: you pay taxes now, and enjoy tax-free income later.

Key Features of a Roth IRA

✅ Contribute with after-tax income

📈 Tax-free growth on investments

💰 Tax-free qualified withdrawals after age 59½

🚫 No Required Minimum Distributions (RMDs)

💼 Ideal for those expecting to be in a higher tax bracket in retirement

Contribution Limits

For 2024, the contribution limits are:

Under age 50: $7,000

Age 50 or older: $8,000 (includes $1,000 catch-up contribution)

💡 Check the IRS for the latest contribution limits.

Income Eligibility

Roth IRA contributions are phased out based on income:

Single filers: Income must be below $146,000 (2024 phase-out starts at $138,000)

Married filing jointly: Income must be below $230,000 (2024 phase-out starts at $218,000)

If your income exceeds these limits, you may consider a Backdoor Roth IRA strategy.

Benefits of a Roth IRA

🛡️ Tax-Free Retirement Income: Withdrawals after age 59½ and after holding the account for at least 5 years are 100% tax-free.

🔄 Flexibility: You can withdraw your contributions (not earnings) at any time, tax- and penalty-free.

🧓 No RMDs: Unlike Traditional IRAs and 401(k)s, Roth IRAs do not require withdrawals at any age, giving you more control and estate planning flexibility.

🧠 Great for Younger Investors: The earlier you contribute, the more time your money has to grow tax-free.

Roth IRA vs. Traditional IRA

Who Should Consider a Roth IRA?

Young professionals in a lower tax bracket

People who value tax-free income in retirement

Individuals who want to avoid RMDs

Anyone with access to earned income under income limits

Opening a Roth IRA

You can open a Roth IRA with most financial institutions, including:

Brokerages (Fidelity, Vanguard, Charles Schwab)

Robo-advisors (Betterment, Wealthfront)

Banks and credit unions

Look for low fees, strong investment options, and intuitive platforms.

Use This Calculator to Plan

👉 Roth IRA Calculator – SmartAsset

Final Thoughts

The Roth IRA is a powerful investment tool that rewards patience and long-term planning. It provides a unique opportunity to lock in today’s tax rate and enjoy tax-free income for life. Whether you're just starting your financial journey or looking to diversify your retirement plan, the Roth IRA deserves a place in your portfolio.

Disclaimer: The information provided on InvestmentIntro.com is for educational and informational purposes only. It should not be considered financial, investment, or tax advice. We are not licensed financial advisors or tax professionals. You should consult with a qualified financial advisor or tax professional before making any financial decisions. All content is provided “as is” without any representations or warranties.

about us | terms of use | privacy policy | contact us

© 2025. All rights reserved.