🏠Traditional IRA: Retirement Growth Tool

💡 Introduction: What Is a Traditional IRA?

A Traditional IRA (Individual Retirement Account) is a powerful retirement savings tool that allows you to contribute pre-tax income (if eligible), invest it, and let it grow tax-deferred until retirement. It’s one of the simplest and most accessible retirement plans, especially for individuals without access to a 401(k) or for those seeking additional retirement savings options.

🔍 How a Traditional IRA Works

Contribute up to a set annual limit using earned income.

Investments grow tax-deferred—you don’t pay taxes on interest, dividends, or capital gains until you withdraw.

Withdrawals are taxed as ordinary income in retirement.

Contributions may be tax-deductible, depending on your income and access to a workplace retirement plan.

🎯 Key Benefits

✅ Tax-Deferred Growth – Let your investments grow without annual tax drag

✅ Tax Deductibility – Potentially reduce taxable income today

✅ Flexible Investment Choices – Choose from stocks, bonds, ETFs, mutual funds

✅ Supplemental Savings – Great for those maxing out a 401(k) or without employer plans

📌 2025 Contribution Limits

Under age 50: $7,000

Age 50 or older: $8,000 (includes $1,000 catch-up)

👉 See current limits on the IRS site

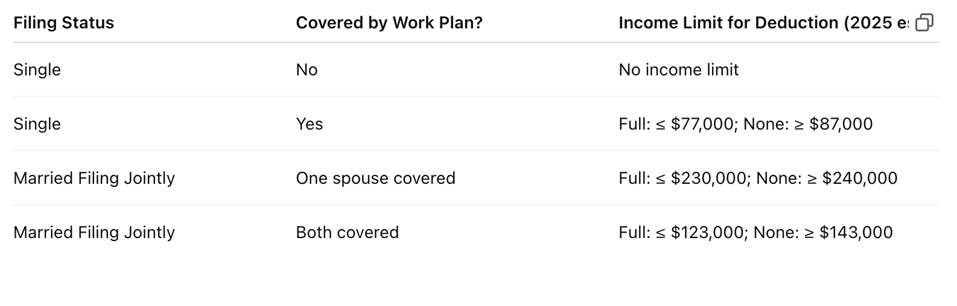

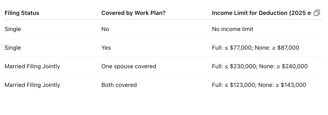

🧾 Tax Deductibility Rules

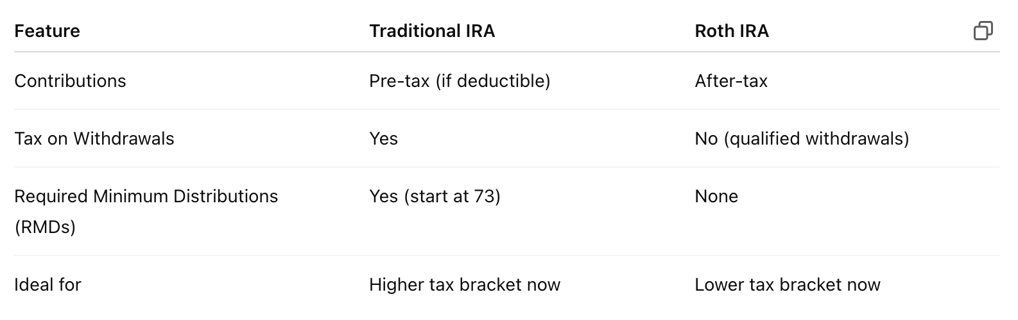

⚖️ Traditional IRA vs Roth IRA

🧮 Traditional IRA Calculator

Use this traditional IRA calculator to view the amount that could be saved using a traditional IRA.

⏳ Withdrawal Rules and Penalties

Withdrawals before age 59½: Subject to 10% penalty + income tax

Exceptions include:First-time home purchase (up to $10,000)

Qualified education expenses

Disability

Medical expenses over 7.5% of AGI

RMDs (Required Minimum Distributions) begin at age 73

Failure to withdraw incurs a 50% penalty on the required amount

🛠️ How to Open a Traditional IRA

Choose a provider: brokerages like Fidelity, Vanguard, Charles Schwab, or robo-advisors

Fund your account with a lump sum or automatic contributions

Choose your investments: index funds, mutual funds, ETFs, or self-managed assets

🔁 Best Practices

📅 Contribute early in the year to maximize compounding

📈 Stay diversified based on your risk tolerance and time horizon

💸 Review yearly: Tax law changes may affect deductibility

💰 Use with other accounts like 401(k)s to boost savings flexibility

❓ Frequently Asked Questions (FAQs)

Q: Can I have both a 401(k) and a Traditional IRA?

Yes, but your deduction eligibility may be limited by income and work plan access.

Q: Can I convert a Traditional IRA to a Roth IRA?

Yes, it’s called a Roth conversion, and it requires paying taxes on converted funds.

Q: Is a Traditional IRA better than a Roth?

It depends on your current and expected future tax brackets. Traditional works well if you’re in a higher tax bracket now.

🧠 Final Thoughts

A Traditional IRA offers a flexible, tax-advantaged way to build retirement wealth. Whether you’re just starting or supplementing other savings, it’s a smart step toward long-term financial freedom. Understanding the rules, benefits, and strategies helps you make informed decisions that compound over time.

Disclaimer: The information provided on InvestmentIntro.com is for educational and informational purposes only. It should not be considered financial, investment, or tax advice. We are not licensed financial advisors or tax professionals. You should consult with a qualified financial advisor or tax professional before making any financial decisions. All content is provided “as is” without any representations or warranties.

about us | terms of use | privacy policy | contact us

© 2025. All rights reserved.